Skadi Loist & Zhenya Samoilova

1. About the Survey

Between May and August 2019, we have conducted a web-based survey among the production companies and filmmakers in our sample. The sample of the project consists of films shown at six selected festivals in 2013: The Berlin International Film Festival (Berlinale), the Festival de Cannes, the Toronto International Film Festival (TIFF), the International Documentary Film Festival Amsterdam (IDFA), the Clermont-Ferrand International Short Film Festival, and the Frameline: San Francisco International LGBTQ+ Film Festival. The purpose of the survey was to collect data on the circulation of films through festivals, as these data are currently available only at the level of small qualitative case studies.

The survey was sent out to 1.332 contacts that corresponded to 1.499 unique films (the questionnaire (Samoilova/Loist 2019) can be accessed here). Films older than 1990 were excluded due to prevalent lack of contact details and low likelihood of response. Contacts were obtained primarily via festival programs. Five percent of contacts were complemented by email addresses gathered from the IMDbPro database. Out of 1.332 contacts 160 proved to be invalid. To incentivize respondents to reply, we offered to enter or update their film data on IMDb; 67 percent of respondents who had data on festivals took up our offer. To reduce the drop-out and ensure high quality responses, we tried to make the survey as short as possible, which forced us to focus on several key questions from the project. Average time to fill out the survey constituted 15 minutes. The survey questions covered the following areas:

- Festival runs & festival markets: we asked to provide the full list of festivals and festival markets that each film attended. Specifically, we asked for full names, date, and location. For the festival, we also asked to enter any awards that a film collected. This information could be given to us via email, by entering directly within a survey, via phone, or an offline form.

- Completeness of information and festival data sources: We asked respondents to subjectively evaluate the completeness of the festival data that they provided to us. Since some filmmakers do not have information about the entire festival run (e.g., due to not keeping records, or not being the sole license owners), we wanted to make potential problems of incompleteness observable. In addition, we asked to specify a source that was used to retrieve the festival data: i.e., whether people used internal documentation, the web, or referred to other sources.

- Finances: questions covered film budget (without marketing costs), marketing costs, festival submission fees and festival screening fees. Furthermore, we included a question about being limited in festival submissions by the available budget.

- Festival consulting: here we asked, if people used services of festival consulting agencies. Although such agencies are becoming widespread, we do not have much empirical evidence about their usage patterns and impact, for instance it is interesting to assess their affiliation with low-budget films.

- Distribution: we included a question on whether a film had any other distribution apart from film festivals, such as theatrical, TV, digital, DVD/Blu-ray, or other types (installations, educational screenings, etc.). If a film was distributed digitally, we asked which platform was used.

- Follow up: We invited people to take part in follow-up qualitative interviews. 60 percent of respondents offered to take part in interviews in the future.

The final sample resulted in 135 unique respondents providing information for 154 unique films (ca. 10 % response rate). Most respondents sent information via email (57 %), followed by entering data directly within the survey (38 %). Only 5 percent of people provided data by phone or filling out an offline form. The vast majority of contacts (95 %) belonged to production companies and producers (some of which were also directors of the projects in question). Five percent of the contacts were email addresses of world sales companies, as no production contacts were available.

We focused mainly on producers, because we assumed, that they would be more motivated to respond due to being directly engaged in the filmmaking and having authority to respond (in contrast to employees of a world sales company, who might depend on the decision of their managers). Of the respondents 26 percent indicated that they were film producers, 16 percent were film directors, and 8 percent stated that they had other roles (e.g. festival managers, distributors, sales and production managers, interns). The other half of respondents (50 %) combined the roles of producer and director.

For 94 films (61 %), respondents were able to provide festival data. For 17 percent of films, festival data were subjectively evaluated as incomplete and for nine percent respondents were not sure, whether the festival data they provided were complete or not. When asked which sources respondents used to provide data on festival runs, for the majority of films (87 %), respondents stated using some internal documentation, for some (19 %) a film website was used (respondents could select more than one source). Other sources used included information provided by sales agent, distributor or filmmaker, and other web resources (IMDb, Facebook, other festival databases, and Google).

2. Looking More Closely at the Survey Sample

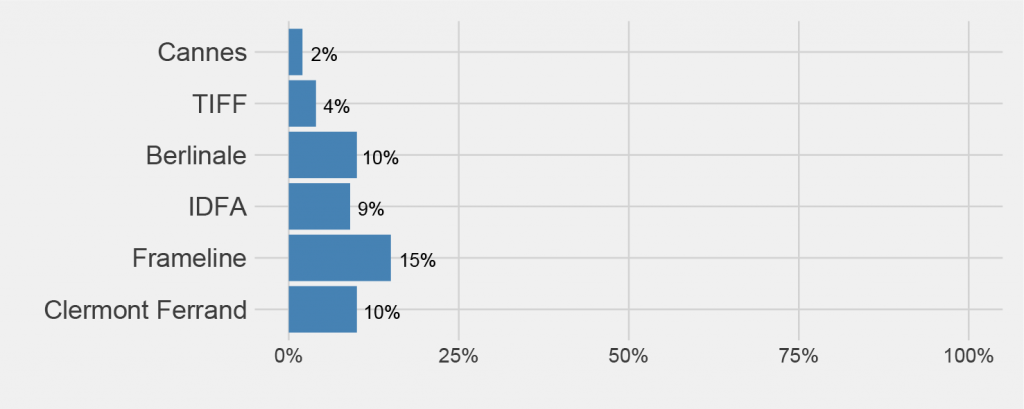

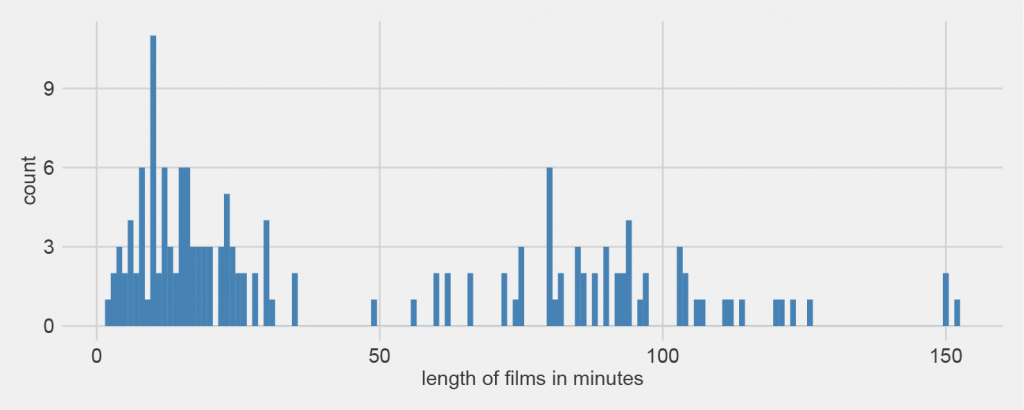

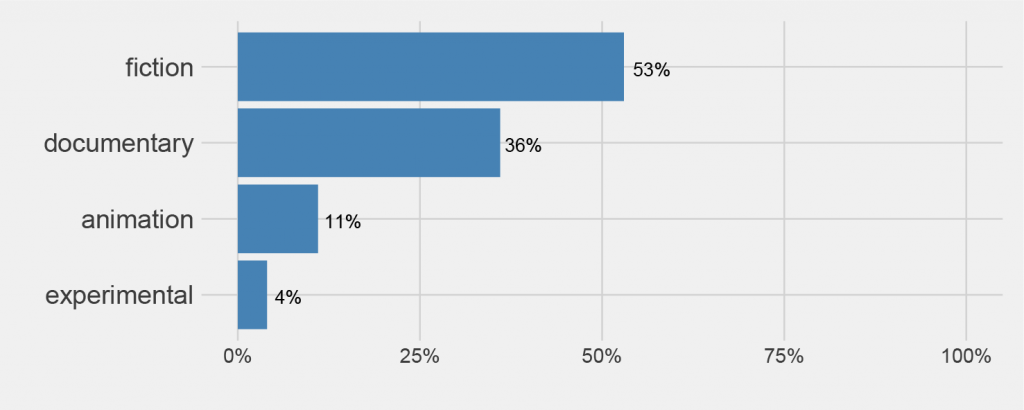

As expected, producers and filmmakers of films shown at A-level festivals – Cannes and TIFF (interestingly except for Berlinale) – are difficult to approach via an online survey. Therefore, films that were screened at IDFA, Frameline and Clermont-Ferrand which are more specialized festivals, are overrepresented (see Fig. 1). More than half of the films (60 %) that we received responses for are shorter than 40 minutes, compared to 54 percent in the original sample (see Fig. 2 for more information on the distribution of film length in the sample). All genres were covered by the survey (53 % fiction, 36 % documentary, 11 % animation, and 4 % experimental; see Fig. 3) with distribution similar to that in the entire sample (55 % feature films, 31 % documentaries, 8 % animation, and 3 % experimental films).

Fig. 1 Percentage of film responses to the survey by festival, n=154 unique films. For Cannes there were only two responses, therefore percentages should be interpreted with caution.

Fig. 2 Distribution of film length (in Minutes) in the survey sample, n=154

Fig. 3 Percentage of film responses to the survey by the film genre, n=147 unique films. Films can have more than one genre. For experimental films n=6, therefore percentages should be interpreted with caution.

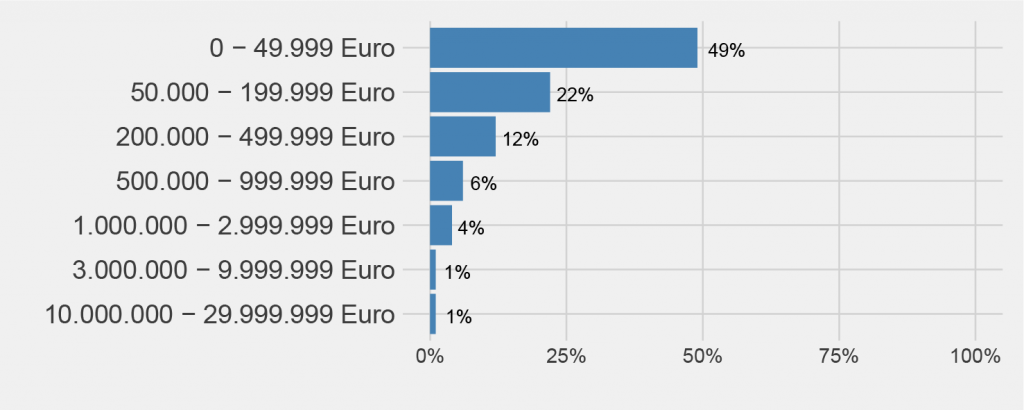

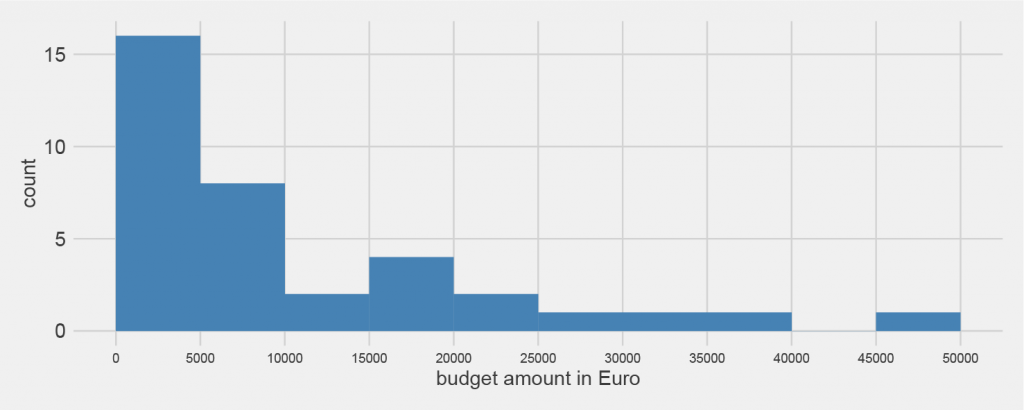

The reported budget of films, excluding the marketing costs, ranges from 76 Euro to 26.515.152 Euro (see Fig. 4). The most frequent budget range reported (49 %) constituted a budget under 50.000 Euro with a median of 6.061 Euro, a minimum budget of 0 Euro and a maximum of 45.455 Euro (see Fig. 5). Two films with the budget above three million Euro stem from the festival sample of TIFF.

Fig. 4 Distribution of reported film budget according to pre-defined ranges (excluding marketing costs) in the survey sample, n=145 unique films. For ranges above one million, sample size is too small, hence percentages should be interpreted with caution.

Fig. 5 Distribution of reported amount of film budget (excluding marketing costs) under 50.000 Euro in the survey sample, n=36 unique films. 60 percent of respondents did not report the approximate budget amount, but responded to the closed question with the pre-defined budget ranges.

3. Festival Runs and Festival Consulting Agencies

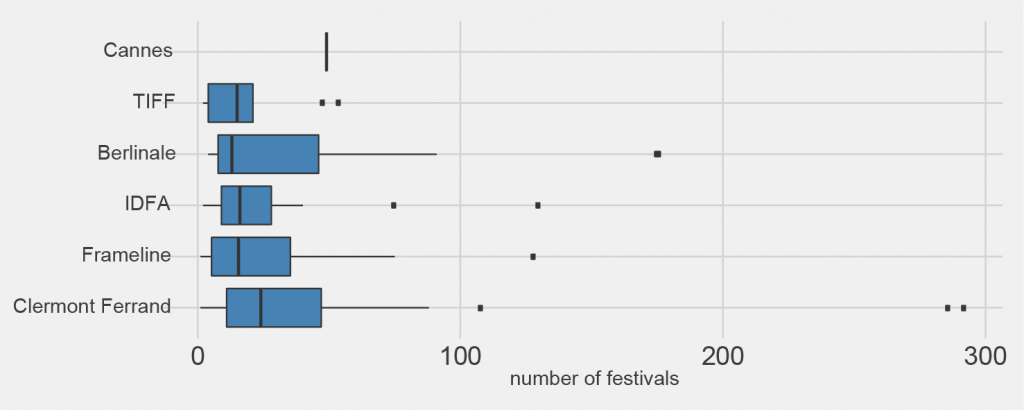

Of the 154 survey respondents, 95 films reported data on festival participation. The minimum amount of festivals included one and the maximum 292 with a median of 19.5 festivals. Figure 6 shows distribution of the number of festivals by the festival sample.

Fig. 6 Number of festivals reported by the sample festival, n=94. For Cannes there were only two responses, therefore percentages should be interpreted with caution.

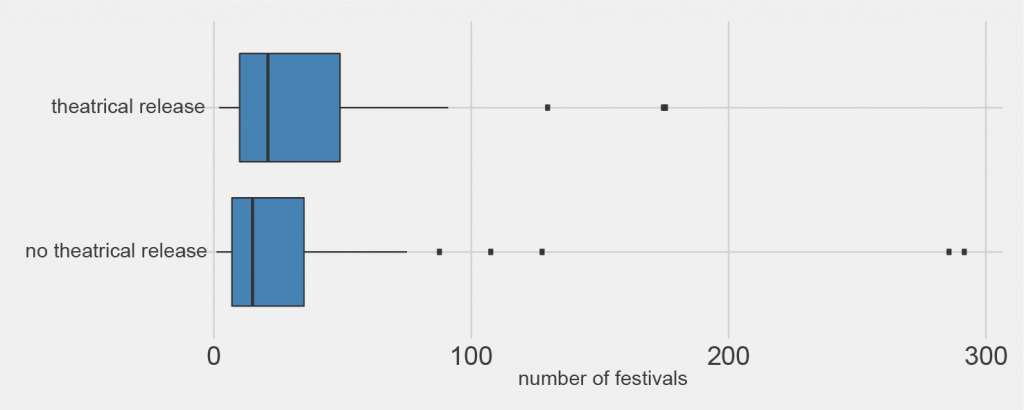

Interestingly, on average films with theatrical release do not report a smaller number of festivals (see Fig. 7). Median for films with theatrical release is 21 festivals, while for those without it is 15 festivals.

Fig. 7 Number of reported festivals by theatrical release, n=94.

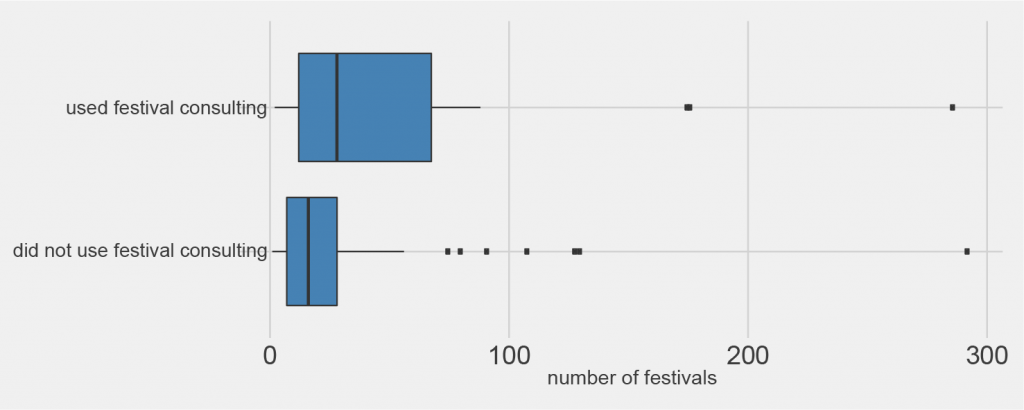

Notably, 42 percent of films used services of consulting agencies to devise a festival strategy or/and to submit to festivals. Films that used consulting services had on average a larger festival run (median=28 festivals), when compared to those without consulting (median=10 festivals) (see Fig. 8). Of course, this does not necessarily mean that consulting agencies are directly responsible for a film going to more festivals. Both, using consulting services and participating in more festivals, could also indicate a higher level of resources available to the film. To shed more light on this, we will have to increase the sample size and control for other factors, such as film and marketing budget.

Fig. 8 Festival run by use of festival consulting services, n=88.

4. Other Types of Film Distribution

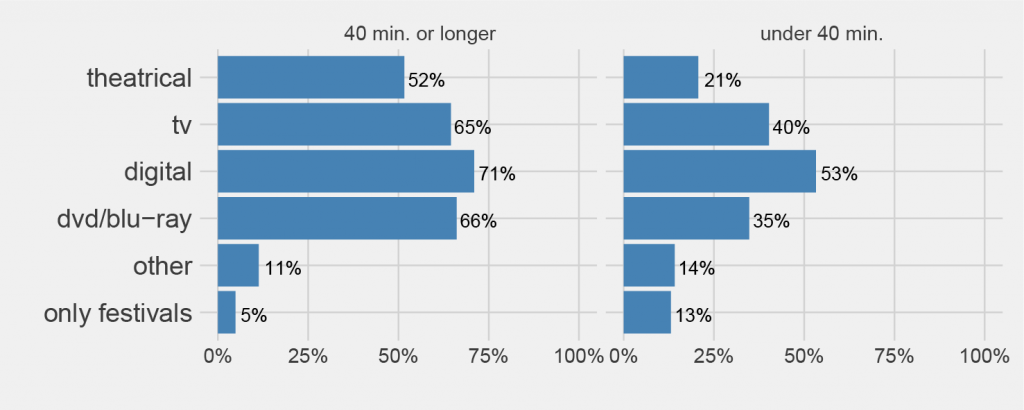

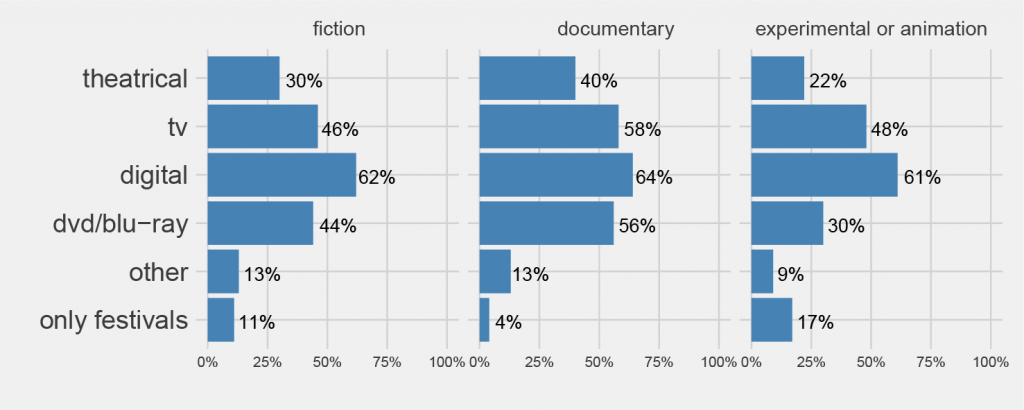

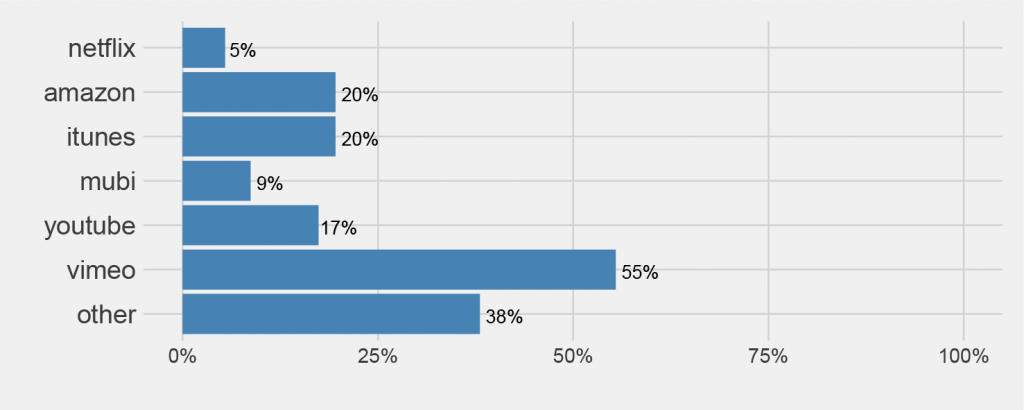

According to the survey, 10 percent of the films were distributed only at film festivals. Other types of distribution included theatrical release (33 % for all films and 70 % for films of 60 minutes and longer), digital distribution (60 %), TV (50 %), DVD and Blu-ray (47 %), and special screenings such as installations, educational screenings, etc. (13 %). Figures 9 and 10 show different types of distribution by film length and film genre. Although digital distribution is quite widespread among the films, only 33 percent of films reported digital distribution on monetized digital platforms. Figure 11 provides more detail on which digital platforms were used by the films.

Fig. 9 Types of distribution by film length, n=154 unique films. Sample size for categories “other” and “only festivals” for films of 40 minutes or longer is too small, therefore percentages should be interpreted with caution.

Fig. 10 Types of distribution by film genre, n=147 unique films. Sample size for categories “other” and “only festivals” is too small, therefore percentages should be interpreted with caution.

Fig. 11 Shares of the used digital platforms among the films that reported digital distribution, n=92. Sample size for categories “Mubi” and “Netflix” is too small, therefore percentages should be interpreted with caution.

5. Film Finances: Marketing, Festival Submission Fees and Screening Fees

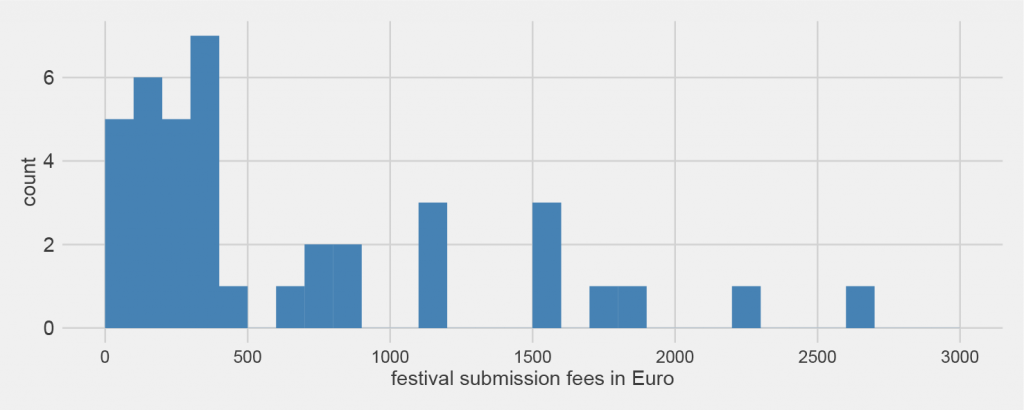

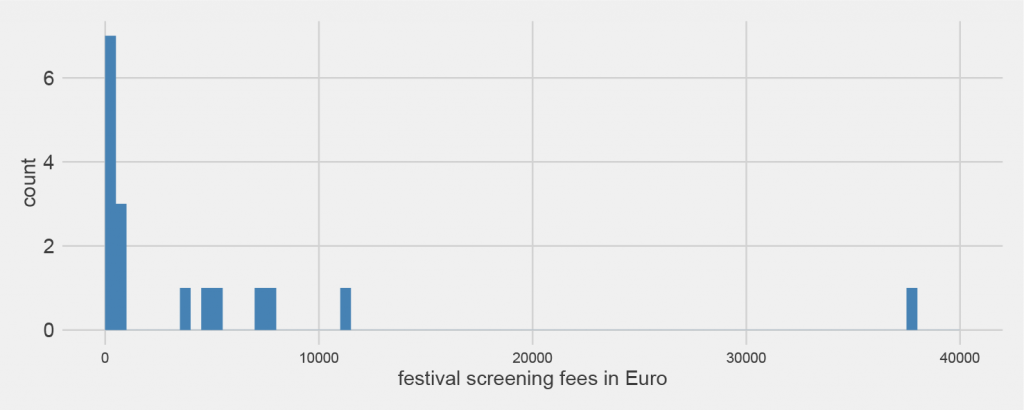

About four-in-ten films (43 %) had a marketing budget, which ranged from 27 to 161.074 Euro with a median of 9.677 Euro. Half of the films (50 %) reported paying festival submission fees at least for one of the festivals, where the film took part. Total costs of submission fees to festivals constituted on average 379 Euro, with a minimum of 30 Euro and a maximum of 2.652 Euro (see Fig. 12). Nearly half of the films (48 %) reported being limited in their festival submission by their budget. In terms of receiving money from the festival run, 42 percent of films received some amount of screening fees: on average 606 Euro, with a reported minimum of 30 and a maximum of 37.879 Euro (see Fig. 13).

Fig. 12 Distribution of approximate amount of festival submission fees (total for all festival submissions), n=146.

Fig. 13 Distribution of approximate amount of festival screening fees (total for all festival screenings), n=137

6. Conclusion

These preliminary results offer a first glimpse into the complex relationship of film variables at play for festival run patterns, expenses and incomes on the festival circuit. In further analyses we strive to delve deeper into these patterns and compare them to existing hypotheses and industry knowledge. In an attempt to offer more solid statistical models, we are currently expanding the survey sample to include additional six years of festival programs, so that the sample covers the range from 2011 to 2017.

Acknowledgements

We would like to thank Deb Verhoeven and Sophie Mathisen for feedback in the development stage of the survey during Skadi Loist’s research stay at the University of Technology Sydney in 2018. We are very grateful to all filmmakers and other team members who took the time to respond to the survey and provide their data to our project.

The project is funded by the Federal Ministry of Education and Research (BMBF) under the number 01UL1710X.

References

Samoilova, Z. & Loist, S. (2019, December 17). Film circulation project questionnaire (Version 2019). Zenodo. http://doi.org/10.5281/zenodo.3581359